One of the most upsetting things that may happen to someone is losing a source of income. Sudden loss of income can make your finances a mess, whether it’s because you lost your job, had to work fewer hours, or had to deal with unanticipated life circumstances. The good news is that you can stay financially stable even if you lose your job if you prepare ahead, use realistic tactics, and make smart decisions. This guide will help you get through tough times, keep your money in check, and even come out stronger on the other side.

Understanding the Effects of Losing Income

It’s crucial to know how losing money will affect your finances before you do anything. If you suddenly lose your job or have your income cut in half, it might be challenging to pay for things like rent, utilities, groceries, and debt payments. If you don’t have a plan, it could lead to stress, bad money choices, or relying on loans with high interest rates. Knowing how something will affect you helps you act fast and wisely. When you accept the circumstance without panicking, you may think about reasonable solutions instead of feeling overwhelmed by the unknown.

Right Away, Look at Your Finances

The first step to keeping things stable is to look at your existing financial situation. Compile a list of all your cash, savings, and other assets that can be converted into cash. Include any possible ways to get money in an emergency, such as severance compensation, unemployment benefits, or help from friends and relatives. Next, write down your most important monthly costs, like rent or mortgage, utilities, groceries, transportation, and debt payments. This test tells you exactly what you need to get by each month. Knowing your resources and responsibilities lets you make smart spending choices and avoid panic buying.

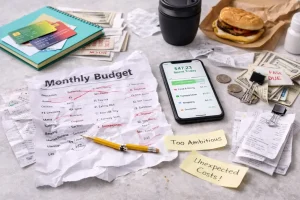

Making a Realistic Budget When Times Are Tough

When you don’t have a lot of money or any money at all, budgeting is essential. Start by taking out things you don’t need and focusing on the things you do need. Set aside money only for housing, utilities, food, transportation, and the least amount of debt payments. To keep things stable, you may have to make short-term compromises like canceling subscriptions, eating out less, or putting off purchases that aren’t necessary. A realistic budget makes sure that your resources go to the most important areas, which helps you stay afloat and get your finances back on track. Keeping track of every dollar spent also helps you be conscious of your finances, which is important when you don’t have any money coming in.

Getting to Your Emergency Funds and Savings

This is the time to use your emergency savings if you have one. A well-funded emergency account functions as a safety net, paying necessary costs without having to take out high-interest loans. Even if your fund isn’t very big, spending it wisely for important payments will keep your finances from getting worse. Put critical costs first and don’t use the fund to buy things you don’t need. If you don’t have an emergency fund, the experience is a good lesson in how important it is to plan for future financial problems. Even if you’re going through a tough time, think about beginning one.

Looking into Ways to Make Temporary Money

Making temporary money can help ease financial stress as you recuperate from losing income. Short-term occupations, freelancing, gig economy gigs, online microtasks, or even selling things you don’t use can help you get the money you need. Local community organizations or government help may also give you short-term help, such as food assistance, unemployment compensation, or help with your bills. Every little bit of money you make helps you stay stable and gives you time to find more permanent answers. Getting temporary income quickly lowers the need for savings and stops financial stress from getting worse.

Talking About Bills and Expenses

One tactic that people often forget about is talking to service providers and creditors. Many businesses have hardship programs, deferred payment plans, or lower rates for people who are temporarily out of work. Tell your landlords, utility companies, insurance companies, and lenders about your circumstances and ask them to be flexible. Negotiating bills not only helps you save money right away, but it also stops late fees, penalties, and service interruptions. Proactive communication shows responsibility and lets you focus on what’s most important.

Cutting Back on Unnecessary Spending

When you lose your job, you may have to make short-term compromises to keep your finances stable. You should stop spending money on things like going out to eat, entertainment, luxury items, or subscriptions that you don’t need. It may feel limiting, but it’s important to put survival and a minimal level of living first. If you move money from non-essentials or savings to necessities, you can make your limited resources last longer and make sure your expenses are paid on time. Over time, spending wisely when times are tough will help you build better financial habits for the future.

Smartly Dealing with Debt

Managing debt is very important when you don’t have any money coming in. If you don’t keep an eye on high-interest debt like credit cards or payday loans, it can easily become out of hand. As you negotiate with your lenders to postpone payments or reduce interest rates, ensure that you only pay the minimum on your essential debts. Don’t take on additional debt with hefty interest rates unless you have to. Putting debt management first stops financial difficulties from getting worse and keeps your long-term stability in place. Handling your debt in a smart way also lowers your stress levels and lets you focus on getting a refund.

Using Help from the Community and the Government

There are many community and government initiatives that can help people who are having trouble with money. Food banks, housing assistance, unemployment benefits, and short-term cash assistance programs can help right now. Using the resources you have is not a sign of failure; it’s a smart way to get things back on track. These programs allow you some breathing room to handle the basics while you look for ways to make more money and minimize costs. Taking the initiative to get help when you need it will help you keep your finances in balance throughout tough times.

Making a Plan of Action for the Short Term

Making a short-term action plan will help you stay organized and on track. List the steps you will take to get your finances back on track, such as making a budget, cutting costs, finding temporary sources of income, and getting help from organizations. Set goals for each week or month that you can reach to keep yourself motivated and on track. A detailed strategy helps you stay calm, gives you a sense of direction, and makes sure you get the most out of your limited resources. Following a strategy and staying disciplined will help you get through financial problems more quickly.

Keeping your Mental and Emotional Health Stable

Money problems can be hard on your mind and emotions. Stress, worry, and confusion can impair clear thinking and sound financial choices. Managing your money is equally as vital as taking care of your emotional health when you lose your job. Keep in touch with friends or family who are there for you, practice ways to deal with stress, and stick to a schedule that helps you feel stable. Emotional resilience helps you make smart choices, keep to your budget, and think of inventive ways to solve problems without getting upset.

Looking at Career and Skill Growth

Losing money can be a chance to rethink your job goals and make yourself more employable. Taking the effort to learn new skills or get certified will increase your chances of finding better-paying jobs in the future. Taking online classes, getting vocational training, or learning new trades can help you get better jobs or freelancing work. Strengthening your skills not only helps you get back on your feet sooner, but it also makes your finances more stable in the long run. Instead of seeing this time as a setback, think of it as an investment in your future safety.

Making Plans for Long-Term Stability

After resolving the immediate issue, focus on ensuring long-term financial stability. To avoid future instability, it’s important to rebuild an emergency fund, find new ways to make money, and stick to a strict budget. Set financial objectives for yourself, such as saving enough money to cover three to six months’ worth of living expenses, paying off high-interest debt, and finding more ways to make money. The things you learn when you lose money can help you make better financial choices and build a stronger base for long-term stability.

Staying Away from Common Mistakes

When you lose money, it’s simple to make mistakes that make your financial stress worse. Some common mistakes are depending too much on high-interest loans, not paying important expenses, taking money out of retirement accounts too soon, or panicking and spending too much. Knowing about these blunders helps you prevent them and stay in charge. Even during challenging times, maintaining discipline and concentrating on realistic solutions can help you achieve your financial goals.

Using Technology to Manage Your Money

When you lose money, technology can be a useful tool. Budgeting tools, cost trackers, and internet banking can all let you see how your money is doing right now. Alerts for bills that are due, automatic transfers to savings accounts, and reminders to keep track of spending all help you stay on track. Technology also makes it easier to find freelance or remote work that pays well. Using these tools wisely helps you stay on top of your finances, stay informed, and stay in charge of your rehabilitation.

Improving Your Financial Mindset

To be stable, you need to have a strong financial perspective. Long-term success comes from seeing problems as transient, working on finding solutions, and staying disciplined. Your mindset affects how you deal with problems, make choices, and plan for the future. Being patient, strong, and proactive will help you avoid long-term instability after losing money. The habits you build at this time, like making a budget, saving money, and putting important things first, can help your finances for years to come.

Conclusion

It’s difficult to keep your finances stable when you lose income, but it’s possible with careful planning, dedication, and a proactive attitude. The first steps are to assess how losing income will affect you, examine your finances, and create a budget you can follow. Using emergency cash, short-term income possibilities, community support, and negotiation strategies can assist in easing acute financial stress. Discipline in spending, managing debt, learning new skills, and making long-term plans will help you get better and stay strong. You may get through losing income and come out stronger financially by using practical tactics and developing a solid financial mindset.

FAQs

1. How soon should I change my budget once I lose money?

Change your budget right away. Put the most important things first, such as housing, utilities, groceries, and the smallest amount of debt you have to pay. Taking action quickly stops financial stress from getting worse.

2. Is it okay to utilize your emergency funds if you lose your job?

Yes, emergency funds are meant to help you when you lose your job. Use them wisely to pay for necessary costs while looking for temporary income and support possibilities.

3. Can short-term work help keep your finances stable?

Of course. Freelancing, gig work, and online jobs can all contribute to your financial stability. Even small amounts of money can expedite your recovery and reduce your reliance on savings.

4. How can I keep my finances from getting worse in the long run when I lose my job?

Don’t borrow money with high interest rates, pay your bills on time, and stick to a budget. Once things are stable again, it’s important to build an emergency reserve and find other ways to make money.

5. What can I do to get ready for losing money in the future?

To be ready for future problems, you should build a strong emergency fund that can cover three to six months’ worth of spending, have more than one source of income, and learn how to be financially responsible.

Aiden Lewis runs pimozoogin.com, where he provides practical and understandable financial tips. He writes articles about Everyday Finance, Financial Stability Tips, Insurance Basics, and Money Habits, with the goal of helping people gain more confidence in managing their finances. He designs his content to enhance financial literacy, foster informed decision-making, and simplify financial matters for everyone. The information provided is for educational and informational purposes only.